Understanding property for sale uae is essential, because it’s a practical map of ownership options, financing realities, and neighborhood dynamics for buyers and investors. This guide explains freehold vs leasehold, where foreigners can own, and the end-to-end process from search to title transfer, with real-world costs and regulatory touchpoints. Backed by current data and Mena Homes listing insights, it reveals where to focus, how to compare options, and what to expect at closing.

Understanding the UAE property landscape for buyers and investors

In the UAE, foreign ownership hinges on the property type and location, with freehold rights giving you title to land and buildings in designated zones and leasehold offering long‑term use without full ownership.

Dubai leads the market in mature freehold zones. For foreigners, several neighborhoods are established freehold targets, including Dubai Marina, Palm Jumeirah, Downtown Dubai, and Jumeirah Lakes Towers (JLT). These areas feature clear title registries and active broker networks, which reduces the friction of first purchases.

Regulatory bodies matter: the Dubai Land Department handles title deeds and transfers, while RERA (Real Estate Regulatory Agency) oversees consumer protections, licensing, and escrow controls on off‑plan deals. For buyers, understanding the timeline from offer to registration, stops last‑minute surprises and narrows the risk of title disputes.

Example in practice: a non‑resident from Europe identifies a two‑bedroom condo in Dubai Marina listed at AED 2.0 million. With a typical 25–30% down payment and a mortgage arranged through a UAE bank, the all‑in cost looks like the price plus around 5–6% in transfer, legal, and registration fees. Include mortgage arrangement fees and an initial valuation. The purchase would proceed under DLD registration, with escrow controls if the property is off‑plan.

A practical constraint to plan for is that not every emirate offers broad freehold rights; Abu Dhabi and others have more limited zones or require leasehold structures. This matters for portfolio strategies where diversification across emirates is appealing but ownership rights vary. In Abu Dhabi, foreign access exists but is more restricted and often tied to project specifics, which can slow closes relative to Dubai.

Key takeaway: Always confirm freehold eligibility for your target area with the official registry (DLD) before bidding, and factor transfer and broker costs into your budget.

Bottom line: focus on Dubai’s mature freehold zones when foreign ownership is a priority, but treat each emirate’s rules as a separate constraint. This clarity prevents overpaying for rights you cannot secure and keeps your investment thesis grounded. Next consideration: verify freehold status in your target area with the DLD through a trusted broker before making an offer.

The step by step buying process in the UAE

Reality check: the UAE buying process follows a disciplined sequence from budget to title transfer. Start with a firm budget that includes not only the price but transfer and registration costs, legal fees, and due diligence. Decide on property type and location early ready homes vs off-plan and align your broker so viewings and negotiations stay focused. Clarity here shortens timelines and reduces surprises.

Define budget and property type and engage a broker. Set a price band, preferred emirate, and property type (apartment, villa, commercial) based on your cash flow and risk tolerance. A broker does more than arrange viewings: they map current UAE listings, verify listing data, and steer you through regulatory touchpoints with Dubai Land Department and RERA, which cuts risk and speeds approvals. Always agree on scope and fees up front.

Mortgage pre-approval. If financing is needed, secure pre-approval early. It fixes your buying ceiling and strengthens offers. Banks require documents and exam eligibility; for non-residents, down payments are higher and LTV tighter. Typical down payments range from 30-50% depending on property type and lender. Expect longer processing times and keep the pre-approval valid for a narrow window.

Offer and MOU. When you find a target, present a formal offer and negotiate. The MOA with the seller sets price, payment schedule, and contingencies, with an upfront deposit typically 5-10% and subject to due diligence and mortgage approval. The contract should spell out cancellation penalties and a transfer deadline to prevent dead ends.

Transfer and registration. After conditions are met, sign the Sale and Purchase Agreement and book a transfer appointment at the land department (Dubai Land Department in Dubai, or the relevant emirate authority). Documents usually include passports, visa copies, the contract, mortgage clearance if any, and sponsor NOC where required. Title deeds are updated on completion.

Due diligence and trade-offs. Off-plan buyers benefit from escrow protections under RERA, but delays happen; ready properties avoid some risk yet can require higher upfront cash. Always verify service charges, HOA rules, and the developer’s credibility. If using a broker, ensure fee clarity and responsible conduct.

Key checkpoints: Define budget and property type; secure mortgage pre-approval; submit offer and sign the MOU; complete transfer at the Land Department; perform final due diligence before funds move.

Financing and cost considerations for buyers

Financing is the gating factor for most property for sale UAE purchases; your borrowing capacity effectively sets the price ceiling and the total cost of ownership. Whether you’re a resident or a foreign buyer, mortgage options and loan-to-value limits vary by lender and property type, so you must anchor your plan in realistic financing scenarios from the start.

Beyond the sticker price, plan for closing and ongoing costs that compound quickly. These not only shape your upfront cash needs but also the affordability of the monthly mortgage over time.

- Mortgage options for residents and non-residents, including typical down payment ranges and required documentation.

- Additional costs such as registration and transfer fees, broker commissions, and valuation or legal fees, plus a buffer for due diligence.

- Currency considerations and how exchange-rate movements affect total cash outlay when funding from abroad; consider hedging options where appropriate.

- Timeline and approvals including mortgage pre-approval, offer to contract, and transfer readiness; processing times can vary by property type and lender.

Concrete example: buying a AED 2.5 million apartment in Downtown Dubai as a non-resident typically involves a 30–40% down payment (AED 0.75–1.0 million). The mortgage could be about AED 1.5 million. Upfront costs might include a 4% transfer fee (AED 100,000), ~2% broker commission (AED 50,000), and a ~0.5% valuation/legals charge (AED 12,500). Ongoing, expect monthly payments in the AED 7,500–8,500 range depending on rate and term.

Important: the headline price is not the total cost. Upfront cash plus ongoing mortgage interest, service charges, and maintenance can dwarf the sticker price over a standard 20–25 year amortization.

Key upfront and ongoing costs for a AED 2.5M property (non-resident): Down payment 30–40% (AED 0.75–1.0M); Transfer fees 4% (AED 100k); Broker commissions 2% (AED 50k); Valuation/Legal ~0.5% (AED 12.5k).

Takeaway: lock in pre-approval early, map out a full cost profile (not just the price tag), and use data-driven tools to compare financing terms against market conditions. When you plan with a complete view, you avoid infotainment-driven decisions and keep the property for sale UAE journey firmly on track.

Hot neighborhoods and investment opportunities in the UAE

Hot neighborhoods are where demand and financing align. In the UAE, coastal urban hubs remain the core of rental activity: Dubai Marina, Palm Jumeirah, and Downtown Dubai consistently attract tenants and short-term visitors. In Abu Dhabi, Yas Island and Saadiyat Island are increasingly pricing in expat families and lifestyle buyers. The value proposition differs by asset class: luxury beachfronts command a premium but also justify higher service charges and maintenance. For buyers, this means pairing lifestyle expectations with observable rental and occupancy trends rather than chasing headlines.

Investment opportunities stack in layers. Core, high-occupancy rentals offer stability; growth corridors tied to new developments promise longer-term upside; and off-plan projects can unlock price discipline if the developer is reputable and escrowed. A pragmatic rule is to look at net yield after HOA and maintenance: mid-range assets in mature markets often produce 4–6% gross yield before tax, with higher potential in well-managed developments and slower turnover. For foreigners, mortgage terms and visa requirements will influence which layer is most practical.

Concrete example: a foreign buyer purchases a 2-bedroom apartment in Dubai Marina for around 2.8 million AED. They put down 30% and finance the rest with a UAE bank; assuming gross rent of about 180,000–200,000 AED per year and annual service charges around 25,000–30,000 AED, the net yield sits in the mid single digits after fees. The property remains highly attractive for tenants and visitors due to proximity to dining, transit, and waterfront amenities.

Trade-offs and risks must be weighed. High entry prices imply sensitivity to interest rate moves and vacancy spikes. HOA charges in luxury towers can compress cash flow, and even reputable off-plan projects carry delivery risk and pricing resets at completion. Limit the risk by sticking to projects with escrow protection, credible developer track records, and clear milestone timelines, and cross check with the Dubai Land Department or RERA guidelines RERA Dubai and the regulatory framework on Dubai Land Department.

- Dubai Marina for high rental density and waterfront lifestyle

- Palm Jumeirah for luxury branding and upscale tenants

- Downtown Dubai for proximity to business and tourism demand

- Yas Island and Saadiyat Island for Abu Dhabi diversification

- Dubai Hills Estate and other gated communities for family tenant appeal

Key takeaway: Focus on established urban hubs with solid occupancy and predictable service charges; diversify with reputable new developments to balance cash flow and long-term value.

Takeaway: anchor initial bets in proven rental hubs, then layer in growth opportunities through credible new developments, supported by careful due diligence and cost awareness. Next, validate these opportunities with up-to-date listings and data in Mena Homes to map exact yields and lead times.

How Mena Homes supports buyers and investors

For buyers and investors exploring property for sale UAE, having a single source of truth matters. Mena Homes provides data-driven search, reliable listing data, and workflows that turn scattered signals into actionable decisions.

What Mena Homes actually provides

The platform wires together UAE real estate listings from multiple sources, applies a verification workflow, and attaches credibility signals to listings and developers. You get timestamped updates, provenance notes, and a consistent data standard that makes cross-comparison feasible rather than guesswork.

- Data-driven search and filters to narrow by price, location, tenure, project status, and delivery timeline.

- Verified listing data with source credibility and update cadence to reduce mispricing and phantom postings.

- Comparative analytics dashboards that let you stack metrics like price per square foot, rental yields, HOA charges, and transfer costs side by side.

- Lead and workflow management to track inquiries, offers, and transfer readiness in one place.

- Marketing and listing management tools for sellers and brokers to improve listing quality, media assets, and speed to market.

Concrete Example: A family office evaluating villas for sale UAE in Abu Dhabi uses Mena Homes to filter by budget, beachfront proximity, and gated community status. Within hours they generate a short list of four viable options with verified ownership documents and transparent all-in cost estimates, then funnel inquiries directly through the platform for faster feedback.

Key takeaway: Reliable listing data across UAE markets reduces due diligence time and strengthens negotiating leverage.

A practical trade-off is that breadth of data can introduce noise if sources aren’t consistently curated. Data provenance matters: if a feed misses updates or misclassifies a tenure type, you’ll chase the wrong comparison. Use defined filters, validate critical items (title, ownership, transfer eligibility), and pair on-platform insights with local counsel and site visits. Mena Homes is the data backbone, not a substitute for on-the-ground verification.

Takeaway: Treat Mena Homesas your data backbone to accelerate research and diligence, then couple it with targeted site visits, local advice, and a clearly defined shortlist to move from inquiry to a confident purchase.

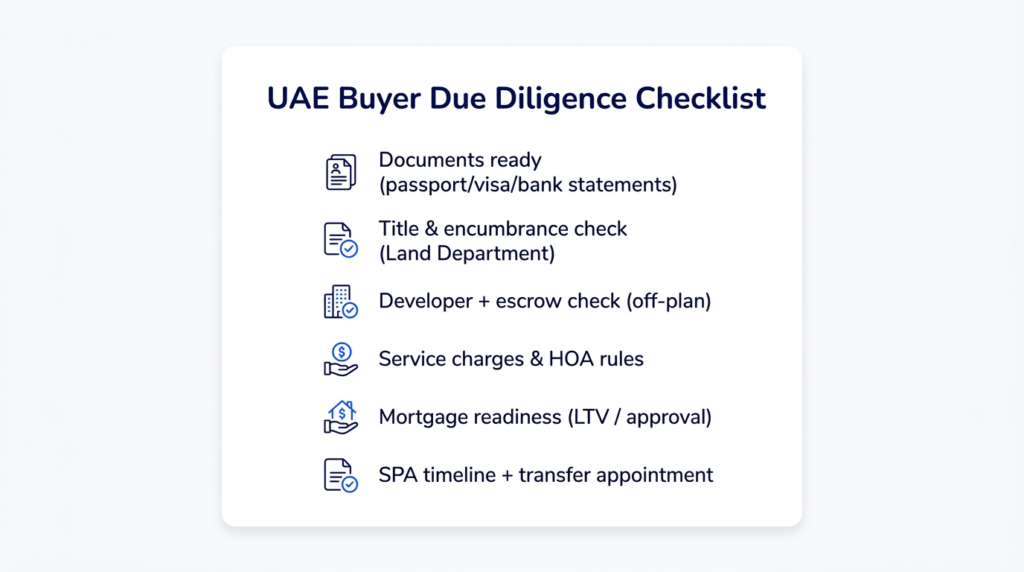

Practical buyer checklist and due diligence

Practical due diligence for property for sale UAE starts before you sign anything. Confirm title status, verify ownership chain, and assess developer credibility early so you can negotiate with clarity, not fear. In real terms, buyers often underestimate the time, documents, and professional checks required to avoid title disputes, hidden charges, or delivery delays. Build a compact, field-ready package you can run through with your broker and, if needed, a lawyer.

A practical checklist in action

- Documentation readiness: Ensure your passport and visa status are current, and gather any sponsor letters, recent bank statements, and proof of income for mortgage discussions if needed.

- Title and encumbrance verification: Check the deed status with the local land department to confirm ownership, freehold rights where applicable, and any liens or unsettled charges on the property.

- Developer and project credibility: For off-plan, demand escrow disclosures, delivery history, and current project status verified by the regulator; for resales, confirm seller’s chain and any previous transfer notices.

- Owners association and maintenance costs: Obtain the latest service charges, HOA rules, upcoming major works, and reserve fund status to avoid surprise bills after purchase.

- Financing readiness: Get mortgage pre-approval, confirm loan-to-value limits, and understand currency implications and potential rate shifts that affect total cost.

- Transfer readiness and contracts: Review the SPA or MOA timeline, ensure funds are ready for transfer, and book the transfer appointment with the land department once all conditions are met.

Concrete example: A foreign buyer targets a beachfront villa in Abu Dhabi. They verify title with the local land authority, request escrow details tied to RERA, and confirm current service charges and the HOA’s reserve plans. They cross-check pricing against similar villas in Mena Homes to avoid overpaying, and align the payment schedule with the regulator-approved milestones to reduce delivery risk.

Off-plan versus ready properties is the classic trade-off. Off-plan can deliver better pricing but introduces completion and specification risk; ready properties reduce timing risk but demand tight checks on current occupancy, service charges, and any ongoing works. Structure deposits and milestone payments to protect equity if the project stalls, and use escrow-based protections where available.

Practical steps to run a two-week due-diligence sprint: 1) assemble documents (passport, visa, sponsor letter, bank statements); 2) pull title and encumbrance status from the relevant authorities (Dubai Land Department and RERA); 3) request developer disclosures for off-plan and verify escrow status; 4) request current service charges, HOA rules, and major works; 5) secure mortgage pre-approval and review currency risk with your lender.

Mena Homes accelerates this workflow by surfacing reliable listing data, flagging potential red flags, and providing dashboards that let buyers and marketers compare properties quickly. Use the platform to confirm ownership type, verify project status, and align price with recent market data before you commit.

Key takeaway: budget a dedicated due diligence window and line item costs (title checks, escrow disclosures, legal fees, and transfer fees) into your purchase plan. The safer the data surface, the stronger the negotiation posture.

Frequently Asked Questions

Reality check: ownership details and processes in the UAE differ by emirate. In Dubai, freehold zones exist and the transfer workflow is well defined, but timing and required documents vary by property type and lender. This FAQ distills the practical answers buyers actually ask to keep you moving toward a decision.

- What is freehold property and who can own it in the UAE? Freehold grants the owner title to land and buildings for an indefinite period and is available to UAE citizens and eligible foreign buyers in designated zones. Check the current freehold map on the Dubai Land Department site or RERA resources Dubai Land Department RERA.

- Can foreigners buy property in the UAE? Yes, in Dubai and Abu Dhabi there are designated freehold zones where foreigners can own real estate; outside those zones ownership is restricted. Confirm eligibility and whether mortgage or visa benefits apply via official sources Dubai Land Department RERA.

- What documents are typically required to buy property in the UAE? A valid passport and visa status, sponsor NOC if required, bank statements for mortgage, and proof of income; have documents translated or legalized as needed for the transfer process.

- How long does the transfer process take in the UAE? Transfers commonly take a few weeks after the MoU is signed and funds are ready; the transfer is executed at the land department and the title deed is issued once settlement completes.

- What are typical costs when buying property in the UAE? Expect transfer and registration charges, broker commissions, valuation and legal fees; total costs commonly total a few percent above the purchase price depending on the deal and developer rules.

- Can foreigners obtain a mortgage in the UAE? Yes, banks offer mortgages to foreigners; down payments typically range from 20 to 50 percent depending on lender and property type; non residents may face higher deposits and stricter income checks.

- How can Mena Homes help with property for sale in the UAE? Our platform provides reliable listing data, market insights, and tools to compare options, track inquiries, and share listings with clients to shorten cycles and improve outcomes.

Key takeaway: budgeting for 4–5% in hidden costs is essential. Align your financing plan early and verify freehold eligibility before making offers.

To move from research to a purchase quickly, start by setting a realistic budget, obtaining mortgage pre-approval, and using a data-driven search on Mena Homes to compare options and verify freehold zones before making an offer.

- Define your budget including 4–5% in additional costs and a contingency for due diligence.

- Secure mortgage pre-approval and gather required documents (passport, visa, income proof, bank statements).

- Build a short list of target freehold zones and property types; use Mena Homes to compare listings and save favorites.

- Engage a reputable broker and prepare for the memorandum of understanding and eventual transfer steps at the land department.